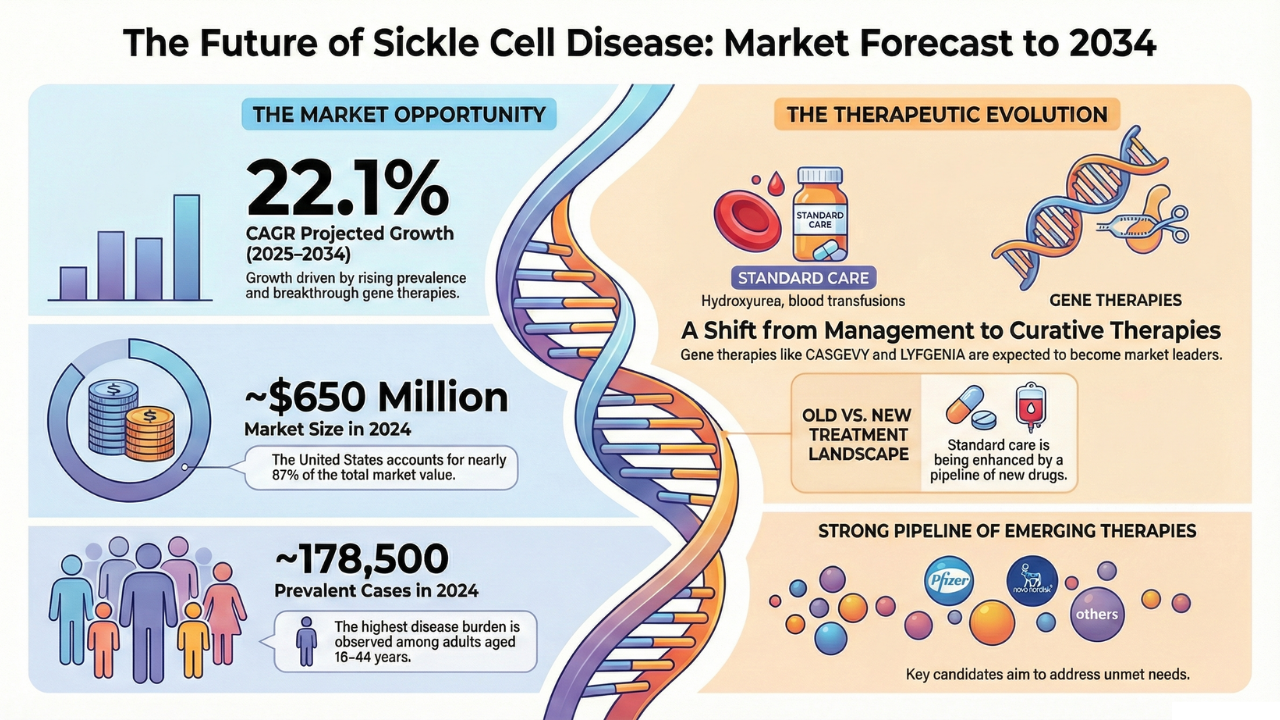

The Sickle Cell Disease (SCD) market is projected to experience remarkable growth through 2034, supported by increasing disease prevalence, improving diagnostic awareness, and rapid advancements in disease-modifying and gene-based therapies. According to DelveInsight, the market is expected to expand at a CAGR of 22.1% across the six major markets (6MM) during the forecast period from 2025 to 2034.

Scientific progress in understanding the underlying pathophysiology of Sickle Cell Disease has catalyzed innovation across both pharmacological and genetic treatment approaches. These advances are reshaping disease management and significantly expanding the therapeutic landscape.

Explore the complete Sickle Cell Disease market forecast and growth drivers through 2034: https://www.delveinsight.com/sample-request/sickle-cell-disease-6mm-market

Sickle Cell Disease Market Overview

DelveInsight’s Sickle Cell Disease Market Insights report provides an in-depth assessment of current treatment practices, emerging therapies, competitive dynamics, and market forecasts from 2020 to 2034 across the United States, EU4 (Germany, France, Italy, Spain), and the United Kingdom.

In 2024, the Sickle Cell Disease market size across the 6MM reached approximately USD 650 million, with the United States accounting for nearly 87% of the total market value, reflecting higher diagnosis rates, stronger treatment uptake, and earlier access to advanced therapies.

A major market-shaping event occurred in September 2024, when all lots of OXBRYTA were withdrawn globally, creating a notable gap in disease-modifying treatment options and accelerating demand for alternative therapies.

Analyze competitive strategies of leading companies in the Sickle Cell Disease market

Sickle Cell Disease Epidemiology Highlights

- The total prevalent population of Sickle Cell Disease in the 6MM was estimated at ~178,500 cases in 2024

- Prevalence is expected to increase steadily through 2034

- The highest disease burden is observed among adults aged 18–44 years, followed by those aged 45–64 years

- The United States represents nearly 73% of diagnosed SCD cases within the 6MM

These epidemiological trends continue to drive sustained demand for both symptomatic and curative Sickle Cell Disease treatments.

Current Treatment Landscape for Sickle Cell Disease

Management of Sickle Cell Disease involves a combination of pharmacologic and supportive therapies aimed at reducing complications and improving quality of life. Standard care currently includes:

- Pain management with opioids, NSAIDs, and acetaminophen

- Blood transfusions and iron chelation therapy

- Antibiotics and nutritional supplements

Disease-modifying therapies include:

- Hydroxyurea (DROXIA) – first-line standard therapy

- ENDARI (L-glutamine)

- ADAKVEO (crizanlizumab)

More recently, gene-based therapies such as CASGEVY and LYFGENIA have emerged as transformational options, with strong potential to redefine long-term outcomes and market leadership by 2034.

Understand unmet needs and patient trends in Sickle Cell Disease across the 6MM

Emerging Therapies Fueling Sickle Cell Disease Market Growth

The Sickle Cell Disease pipeline is highly active, with multiple late-stage and mid-stage candidates targeting diverse disease mechanisms. Key emerging therapies include:

- Osivelotor (GBT-601) – Pfizer

- Inclacumab – Pfizer

- Etavopivat – Novo Nordisk

- Mitapivat – Agios Pharmaceuticals

- Pociredir – Fulcrum Therapeutics

- CRISPR by Design – Scribe Therapeutics

These therapies aim to address unmet needs by improving hemoglobin stability, reducing vaso-occlusive crises, enhancing red blood cell metabolism, or offering curative gene-editing solutions.

Sickle Cell Disease Competitive Landscape

The sickle cell disease (SCD) competitive landscape is rapidly evolving, driven by advances in disease-modifying therapies, gene therapies, and supportive care innovations. Established players such as Novartis, Pfizer, and Bristol Myers Squibb continue to expand their SCD portfolios, while emerging biotechs like Bluebird Bio, Vertex Pharmaceuticals, CRISPR Therapeutics, and Beam Therapeutics are advancing curative gene-editing and gene-addition approaches. Increasing focus on fetal hemoglobin induction, anti-adhesion therapies, and one-time curative treatments is intensifying competition. Strategic collaborations, regulatory momentum, and strong clinical pipelines are reshaping the future of SCD treatment.

Key Companies in the Sickle Cell Disease Market

The Sickle Cell Disease market is characterized by strong competition and innovation across biotech and large pharmaceutical players. Prominent companies actively shaping the market include:

- Pfizer

- Agios Pharmaceuticals

- Novo Nordisk

- Fulcrum Therapeutics

- Scribe Therapeutics

- Sanofi

- Vertex Pharmaceuticals

- CRISPR Therapeutics

- Bluebird Bio

- Emmaus Life Sciences

Gene therapies CASGEVY and LYFGENIA are expected to emerge as market leaders, significantly influencing treatment paradigms and revenue growth across the 6MM by 2034.

Recent Developments in the Sickle Cell Disease Market

- November 2025: Fulcrum Therapeutics announced upcoming Phase Ib PIONEER trial data for pociredir at ASH 2025

- August 2025: Pfizer reported Phase III THRIVE-131 results for inclacumab, which did not meet its primary endpoint

- March 2025: Editas Medicine discontinued EDIT-301 following challenges in securing a commercial partner

- January 2025: Scribe Therapeutics achieved a research milestone in its collaboration with Sanofi

- 2026 Outlook: Mitapivat Phase III results may support a U.S. commercial launch

Access in-depth clinical trial insights for next-generation Sickle Cell Disease treatments

Sickle Cell Disease Market Outlook

With rising prevalence, increasing awareness, expanding access to specialty care, and the anticipated approval of next-generation therapies, the Sickle Cell Disease market is poised for significant long-term growth. The convergence of oral therapies, biologics, and gene-editing platforms is expected to transform the standard of care and create substantial commercial opportunities.